The federal law was announced in 2019, this year UAE courts have started accepting cases

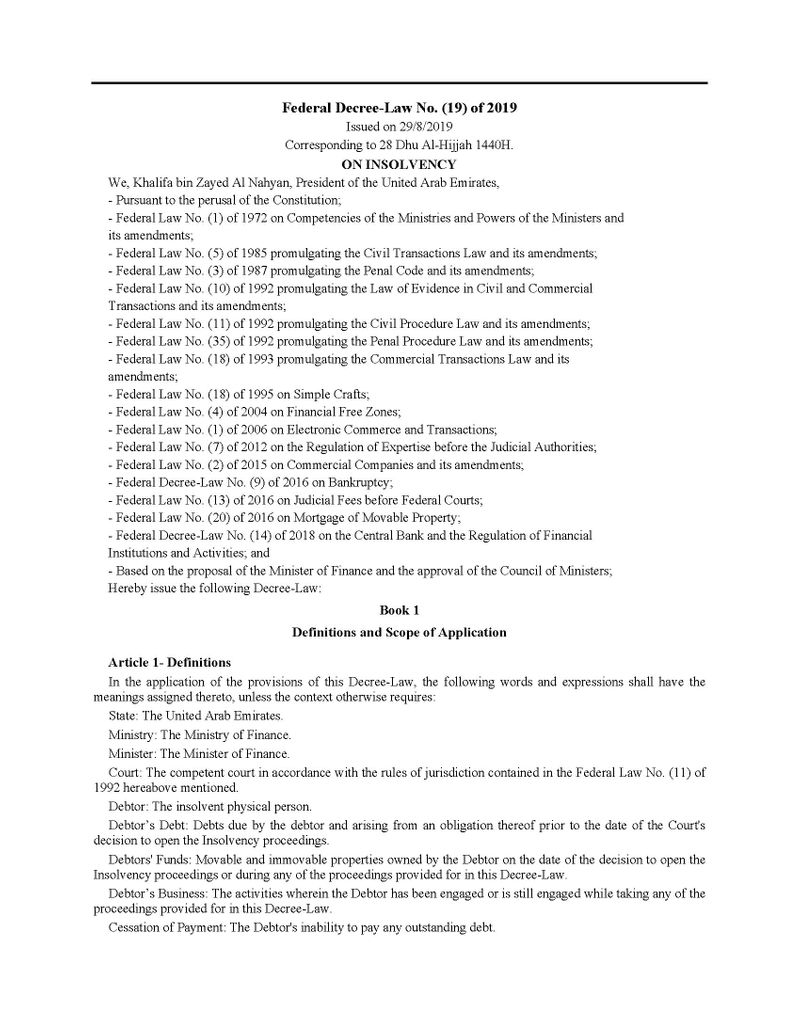

Dubai: The UAE took a landmark decision last year, when the Federal Decree Law No. (19) of 2019 on insolvency was issued. While earlier, the bankruptcy law covered companies struggling financially, the new law promised to assist individuals who were overwhelmed by debt, unable to pay.

Speaking to Gulf News, Jihene Arfeoui, a Dubai-based legal researcher, said that the law came into force earlier this month (January, 2020), calling it the year of economic and social development and aspiration for a happier and more stable country.

“The courts have started taking cases from individuals under the new law from this month. The insolvency law has set out clear and easy-to-apply rules for collecting bad debts and rehabilitating the financial position of the debtor, which also encourages loaning individuals or creditor banks,” she said.

What is the insolvency law?

Distinguishing the new law from Federal Law by Decree No. (9) of 2016 on Bankruptcy, Jihene said: “Contrary to the federal bankruptcy law, the insolvency law includes civilians who are not merchants whose financial difficulties have prevented them from paying their debts and discharging their financial receivables – the insolvency law has set out clear and easy-to-apply rules for collecting bad debts and rehabilitating the financial position of the debtor, which increases the credibility of creditor banks in loaning individuals.”

The courts have started taking cases from individuals under the new law from this month. The insolvency law has set out clear and easy-to-apply rules for collecting bad debts and rehabilitating the financial position of the debtor, which also encourages loaning individuals or creditor banks.

How does the law help individuals settle their financial debts?

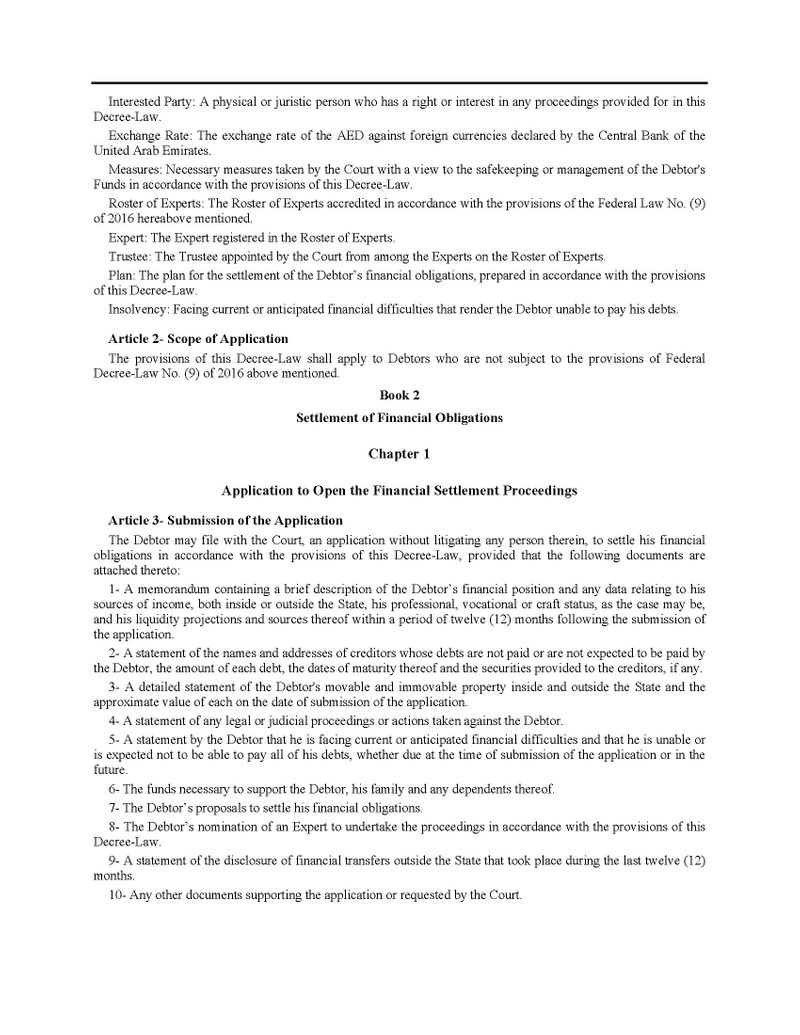

In Book 2 of the law, titiled ‘Settlement of financial obligations’ the articles lay out a detailed and clear process that needs to be followed by the debtor.

“As per the law, this is the procedure for settlement of all debts: The debtor goes to the court and opens a case, not against anyone specifically, but instead as a request to the court to help him settle his debt. He should submit all the documents listed and pay the professional fees. The court will then issue a decision, appointing an expert to start the procedures,” Jihene said.

“There can be one or more than one expert, he should start just after five days when he receives the notification from the court. He will do many things like looking at the document submitted by the debtor, calculate the amount of debt and prepare his reports.

“Regarding the settlement plan, the expert should work with the debtor himself. When he prepares the plan, he should give a copy to the creditor to give their opinion and put it in the court within 22 days from the date of appointment of the expert.”

Does it stop criminal or civil cases against the debtor?

According to the Dubai-based legal researcher, it does.

“The law stipulated that during the insolvency and liquidation procedures, it is not permissible to initiate or pursue any lawsuits or take legal or judicial measures against the debtor, as the issuance of the decision to open the insolvency and liquidation procedures entails stopping the entitlement of legal or contractual benefits to the debtor,” she said.

In Article 7, the law states: “The Court’s decision to accept the Debtor’s application for the settlement of his financial obligations shall result in the suspension of the creditor’s right to request execution against the Debtor’s Funds or the opening of his Insolvency and liquidation proceedings. Such suspension shall continue during the period of the Debtor’s proceedings of the settlement of financial obligations.”

By facilitating the process of settling debts and protecting the debtor against any additional criminal or civil claims, the law aims to provide relief to individuals suffering from crippling debt.

How can I apply for insolvency?

Chapter 1, titled ‘Application to Open the Financial Settlement Proceedings’ lays down the process an individual needs to follow.

Step 1 – Approach the court

You need to raise the case with a court in the UAE.

Step 2 – Prepare the documents

You would need to provide the following documents as part of your application:

- A memorandum containing a brief description of the Debtor’s financial position and any data relating to his sources of income, both inside or outside the State, his professional, vocational or craft status, as the case may be, and his liquidity projections and sources thereof within a period of twelve (12) months following the submission of the application.

- A statement of the names and addresses of creditors whose debts are not paid or are not expected to be paid by the Debtor, the amount of each debt, the dates of maturity thereof and the securities provided to the creditors, if any.

- A detailed statement of the Debtor’s movable and immovable property inside and outside the State and the approximate value of each on the date of submission of the application.

- A statement of any legal or judicial proceedings or actions taken against the Debtor.

- A statement by the Debtor that he is facing current or anticipated financial difficulties and that he is unable or is expected not to be able to pay all of his debts, whether due at the time of submission of the application or in the future.

- The funds necessary to support the Debtor, his family and any dependents thereof.

- The Debtor’s proposals to settle his financial obligations.

- The Debtor’s nomination of an Expert to undertake the proceedings in accordance with the provisions of this Decree-Law.

- A statement of the disclosure of financial transfers outside the State that took place during the last twelve (12) months.

- Any other documents supporting the application or requested by the Court.

Failure to Complete the Required Data

According to the law, “If the Debtor is unable to provide any of the documents or data required in accordance with the provisions of Article (3) of this Decree-Law, he shall state the reasons therefor in his application. If the Court deems that the documents submitted are not sufficient to decide on the application, it may grant the debtor a time-limit for the submission of any additional data or documents.”

Step 3 – Payment of Fees and Expenses

The exact amount of fees is specified by the court, after assessing the expertise fees and fees of the judicial proceedings. If the debtor is not in a position to make the payment immediately, the law has provisions for delaying the payment.

Step 4 – Measures to preserve debtor’s funds

The Court may decide to take the necessary measures to preserve the Debtor’s Funds while the case is being processed.

Step 5 – Court decides on the application

Within five days of the application being submitted to the court, the court will decide on whether it will accept the application or not. If the application is accepted to settle the individual’s financial obligations.

If the court rejects the application, the individual can take the application to the Court of Appeal. The decision issued in the appeal shall be considered final.

Step 6 – Assigning an expert

The court will then assign an expert, or experts, to the case. The specific regulations related to the selection and assigning of the expert are stated in Article 8 of the law.

Step 7 – Creditors submit their documents

Next, the creditors would need to hand over their debt documents to the expert, along with the necessary statements and collaterals.

Step 10 – Expert completes his report

In 20 days, unless the court grants an extension, the expert will submit a detailed report, clearly laying down the dues and the details provided in the documents of the debtor and creditors.

Step 11 – Court audits the report

The court will then audit the report and if it deems necessary will instruct the expert to create a payment plan to settle the financial obligations of the debtor.

What are the cases in which the application can get rejected?

According to the law, these are the conditions that can lead to the rejection of the application

1- If it is established to the Court that the Debtor has carried out any action or refrained therefrom with a view to concealing or destroying any part of its funds.

2- If the Debtor has provided false statements on his debts, rights or funds.

3- If the Debtor has ceased to pay any of his debts on the maturity date thereof for more than fifty (50) consecutive working days, as a result of his inability to pay such debts.

Step 12 – Preparing the repayment plan

Articles 13 to 20 of the law lay down the detailed process of approval, voting and clearance from all concerned parties to finalise on a repayment plan.

Step 13 – Implementation of the financial settlement plan

Articles 21 to 24 detail how the expert, who is now in a position of supervising the execution of the plan, would implement the plan. This would include sale of any property held by the debtor and provide regular updates to all parties concerned on the repayment of dues. It is also possible that during the implementation of the plan, the expert finds it necessary to make amendments to the plan. In such a scenario, the process is laid out in Article 24.

Step 14 – Termination, Expiry and Nullity of the Financial Settlement Proceedings Plan

In case the debtor clears all dues as per the plan, the plan shall be completed. However, if the debtor still fails to clear his dues, the law goes on to state how the court and the appointed expert can go on to start insolvency proceedings, which include but are not limited to sale of assets.

This is the complete text of the law:

{kind=link}