Dubai: Outlook for GCC banks in 2021 is expected to remain negative according to rating agency Moody’s.

The 2021 outlook for GCC banks is driven by subdued economic growth, continued business disruption related to the coronavirus outbreak, and fiscal consolidation that is pressuring loan quality and profitability, Moody’s said in a report.

Lower oil revenues have reduced deposit inflows from governments, the banks’ largest depositors, slightly squeezing their funding costs, while the deterioration of sovereign credit profiles could weaken governments’ capacity to support banks.

Asset quality

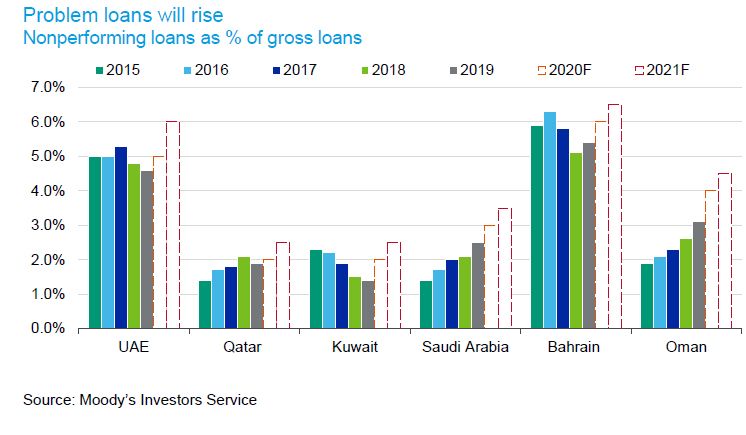

Loan performance will be under pressure as subdued growth in the non-hydrocarbon economy weighs on borrowers’ loan repayment capacity. Loan repayment holidays as part of measures to combat Covid19 pandemic have kept non-performing loans at low levels so far, but we expect these to rise.

“Pressure on loan quality and profitability are the main drivers behind our negative outlooks on all six banking systems in the countries of the Gulf Cooperation Council,” said Ashraf Madani, a Moody’s Vice President – Senior Analyst and the report’s co-author.

“Despite the negative outlooks, GCC banks’ creditworthiness remains in many cases strong, particularly for those in Kuwait, Saudi Arabia and Qatar.”

Loan repayment holidays to support borrowers through the coronavirus crisis will delay recognition of nonperforming loans. These will rise, however, by end of 2020 and in 2021 as payment holidays expire and some borrowers, hit badly by the pandemic, become insolvent.

Loan quality in Qatar and Kuwait will fare best through the economic downturn. “We expect loan performance to suffer more severely in UAE and Bahrain,” said Madani.

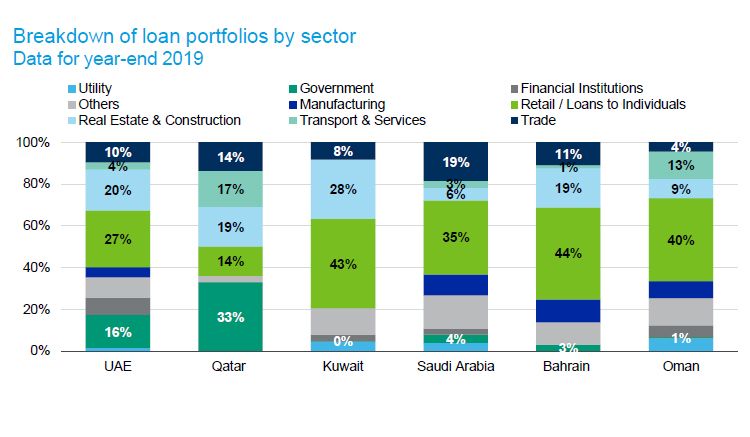

Real-estate, construction, hospitality and retail sectors will be hit hardest by the pandemic and will generate the greatest number of problem loans and large loan restructurings across the region. Moody’s said GCC banks’ loan books lack diversification and are concentrated on a few large borrowers and certain sectors. This increases their vulnerability in the event of a default by one of them or to a shock in a specific sector.

Weak profitability

Profitability will weaken as provisioning needs rise and yields fall. Moody’s expects an average return on assets of around 1 per cent to 1.2 per cent for 2020 and 2021, down from around 1.5 per cent for 2019. Higher loan-loss provisioning requirements will weaken profitability but the banks will remain profitable. Additionally, margins will remain under pressure from lower interest rates. Banks will keep tight controls over costs.

Total assets of 18 listed national banks rise to AED3 trillion by end of June

A slew of mergers across the region that started in 2016 will continue, driven by subdued economic growth, stiff competition and an over-abundance of small banks.

The negative outlook could turn stable if there is strong rebound in economic growth and a relaxation of fiscal consolidation measures, as well as a return to high levels of government spending. A significant increase in oil prices which boosts investor confidence would also be positive, as would the end of the pandemic and a resumption of normal activities.

Strong capitalisation

GCC banks’ capital adequacy will be stable next year because most banks will remain moderately profitable and loan growth will be subdued. Potential regulatory controls may threaten dividend payouts. Strong capital provides sizeable loss-absorption potential. Banks are largely funded by deposits, with governments their largest depositors. Lower government deposit inflows due to reduced oil revenues may push funding costs slightly higher. High liquid buffers mostly in the form of money market and government securities, will mitigate funding concentration risk.

{kind=link}